Market Research Industry Today

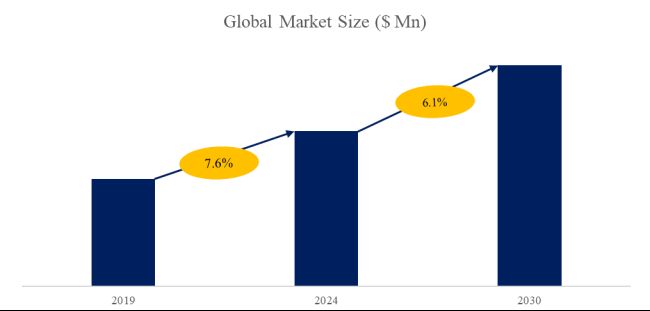

Electronic Grade Dichlorosilane DCS (SiH2Cl2) Industry Research:the global Electronic Grade Dichlorosilane DCS (SiH2Cl2) market size is projected to reach USD 1.18 billion by 2030,

According to the new market research report “Electronic Grade Dichlorosilane/DCS (SiH2Cl2) - Global Market Share and Ranking, Overall Sales and Demand Forecast 2024-2030”, published by QYResearch, the global Electronic Grade Dichlorosilane DCS (SiH2Cl2) market size is projected to reach USD 1.18 billion by 2030, at a CAGR of 5.6% during the forecast period.

- Global Electronic Grade Dichlorosilane MarketSize(US$ Million), 2019-2030

Source: QYResearch, "Electronic Grade Dichlorosilane/DCS (SiH2Cl2) - Global Market Share and Ranking, Overall Sales and Demand Forecast 2024-2030”

- Global Electronic Grade Dichlorosilane Top5Players Ranking and Market Share (Ranking is based on the revenue of 2023, continually updated)

Source: QYResearch, "Electronic Grade Dichlorosilane/DCS (SiH2Cl2) - Global Market Share and Ranking, Overall Sales and Demand Forecast 2024-2030”

According to QYResearch Top Players Research Center, the global key manufacturers of Electronic Grade Dichlorosilane DCS (SiH2Cl2) include Shinetsu, Nippon Sanso, etc. In 2023, the global top three players had a share approximately 68.0% in terms of revenue.

- Electronic Grade Dichlorosilane,Global Market Size, Split by Product Segment

Source: QYResearch, "Electronic Grade Dichlorosilane/DCS (SiH2Cl2) - Global Market Share and Ranking, Overall Sales and Demand Forecast 2024-2030”

In terms of product type, currently ≥99.9% is the largest segment, hold a share of 76.2%.

- Electronic Grade Dichlorosilane,Global Market Size, Split by ApplicationSegment

Source: QYResearch, "Electronic Grade Dichlorosilane/DCS (SiH2Cl2) - Global Market Share and Ranking, Overall Sales and Demand Forecast 2024-2030”

In terms of product application, currently Semiconductor is the largest segment, hold a share of 76.2%.

- Electronic Grade Dichlorosilane,Global Market Size, Split by Region

Source: QYResearch, "Electronic Grade Dichlorosilane/DCS (SiH2Cl2) - Global Market Share and Ranking, Overall Sales and Demand Forecast 2024-2030”

Market Drivers:

Semiconductor Industry Growth: As dichlorosilane is a critical precursor in the production of high-purity silicon for semiconductors, the growth of the semiconductor industry directly impacts the demand for EDCS. With the increasing demand for electronic devices like smartphones, tablets, and other smart gadgets, there is a corresponding rise in the demand for high-purity silicon, thereby driving the EDCS market.

Advancements in Electronics: Technological advancements, such as the Internet of Things (IoT), artificial intelligence (AI), and 5G communication, require increasingly sophisticated semiconductor devices. This drives the need for higher purity materials like EDCS in semiconductor manufacturing processes to meet the stringent performance requirements of these technologies.

Miniaturization and Integration: The trend toward miniaturization and integration of electronic components demands higher purity materials to ensure the reliability and performance of semiconductor devices. EDCS is essential for the production of ultra-pure silicon, which is crucial for manufacturing smaller and more efficient electronic components.

Geographical Expansion of Semiconductor Manufacturing: The expansion of semiconductor manufacturing facilities, particularly in regions like Asia-Pacific, further drives the demand for EDCS. Countries like China, South Korea, and Taiwan are investing heavily in semiconductor fabrication facilities, leading to increased consumption of EDCS in these regions.

Stringent Quality Standards: With the semiconductor industry requiring materials of the highest purity, there is a growing emphasis on quality standards and specifications for EDCS. Manufacturers must meet these stringent requirements to ensure the reliability and performance of semiconductor devices, driving innovation and investment in EDCS production processes.

Environmental Regulations: Environmental regulations regarding the use of certain chemicals in semiconductor manufacturing processes may also influence the EDCS market. Companies may seek alternatives or invest in cleaner production methods, affecting the demand dynamics of EDCS.

Restraint:

Overcapacity: The production capacity for EDCS may sometimes outstrip demand, leading to an oversupply situation. This can occur due to expansions or new entrants in the market driven by optimistic forecasts of semiconductor demand growth. Overcapacity can result in downward pressure on prices, reduced profit margins, and increased competition among EDCS manufacturers.

Market Volatility: The semiconductor industry, which is the primary consumer of EDCS, is subject to cyclical demand patterns and market volatility. Economic downturns, shifts in consumer demand for electronic devices, or geopolitical tensions can lead to fluctuations in semiconductor demand. Consequently, EDCS producers may face challenges in predicting and responding to changes in market conditions, leading to inventory build-up or underutilized production capacity.

Long Lead Times and Capital Intensity: Establishing new EDCS production facilities or expanding existing ones requires significant capital investment and long lead times. This can pose a barrier to entry for new players and limit the ability of existing producers to quickly adjust production levels in response to changing market dynamics. As a result, the market may experience periods of overcapacity or underutilization of capacity, exacerbating the risk of oversupply.

Technological Advances and Substitution: Technological advances in semiconductor manufacturing processes or the development of alternative materials could pose a threat to the demand for EDCS. For example, emerging technologies such as gallium nitride (GaN) or silicon carbide (SiC) may offer advantages over traditional silicon-based semiconductors, reducing the need for high-purity silicon precursors like EDCS.

Regulatory and Environmental Constraints: Regulatory requirements related to environmental protection and workplace safety could increase compliance costs for EDCS producers. Additionally, concerns about the environmental impact of semiconductor manufacturing processes may drive demand for cleaner and more sustainable alternatives, potentially affecting the market for EDCS.

Opportunity:

Rising Demand for Semiconductor Devices: The increasing adoption of electronic devices across various industries, including automotive, healthcare, aerospace, and consumer electronics, is driving the demand for advanced semiconductor devices. EDCS is a crucial precursor in the production of high-purity silicon, which is used in the fabrication of integrated circuits, microchips, sensors, and other semiconductor components.

Advancements in AI, IoT, and 5G: Technologies such as artificial intelligence (AI), the Internet of Things (IoT), and 5G communication are driving the need for more powerful and efficient semiconductor devices. These applications require high-performance chips with enhanced computing capabilities, which, in turn, necessitates the use of high-purity silicon produced using EDCS.

Miniaturization and Integration: The trend toward miniaturization and integration of electronic components is creating opportunities for EDCS manufacturers. As electronic devices become smaller and more complex, the semiconductor industry demands higher purity materials to ensure the reliability and performance of integrated circuits and other electronic components.

Emerging Semiconductor Markets: Emerging markets, particularly in Asia-Pacific and Latin America, present significant growth opportunities for the semiconductor industry. Countries like China, India, Brazil, and South Korea are investing heavily in infrastructure development, industrialization, and technological innovation, driving the demand for semiconductor devices and, consequently, EDCS.

Green Technologies and Renewable Energy: The transition toward green technologies and renewable energy sources, such as solar photovoltaics (PV) and electric vehicles (EVs), is fueling demand for semiconductor devices used in solar panels, batteries, and power electronics. EDCS is essential for producing high-purity silicon wafers used in solar cells and other renewable energy applications.

Quality and Performance Requirements: The semiconductor industry's stringent quality and performance requirements create opportunities for EDCS manufacturers to innovate and develop advanced production processes. Improvements in EDCS purity, consistency, and reliability can enhance the performance and yield of semiconductor manufacturing processes, thereby strengthening the competitive position of EDCS suppliers.

Partnerships and Collaborations: Collaboration between EDCS manufacturers, semiconductor companies, and research institutions can drive innovation and market growth. Partnerships focused on developing new materials, processes, and applications for high-purity silicon can unlock new opportunities and expand the EDCS market's reach.

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting, industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US) 0086-133 1872 9947(CN)

EN: https://www.qyresearch.com

JP: https://www.qyresearch.co.jp

Share on Social Media

Other Industry News

Ready to start publishing

Sign Up today!